1. Introduction

Impressum 5.20 - Beta version

Publisher: International Federation for the Economy for the Common Good e.V.

Author: Matrix Development Team

Release: 2026-04-13 v0.84 => Click here for the 0.85 version

Version 5.2 editors: Marta Avesani, Walter Kern, Sabine Lehner, Renata Sommer, Wolfram Sommer.

Previous editors: Angela Drosg-Plöckinger, Manfred Blachfellner, Monika Culka, Susanna Fieber, Peter Frank, Gerd Hofielen, Lutz Knakrügge, Sigrid Koloo, Carlos Lopez-Monllor, Susanna Mur, Pedro Olazabal, Ulrich Rücker, Karla Schimmel, Regina Sörgel, Lea Strub, Moritz Teriete, Christine Unterrainer, Carlos Adolfo Viale.

With thanks to: Christian Felber, Christian Loy, Christian Rüther, Christoph Spahn, Dominik Sennes, Eva Wagner.

Stakeholder feedback team: Sabine Lehner, Renata Sommer, Carlos Adolfo Viale.

Our heartfelt thanks go to everyone who sent their feedback and suggestions for revising this manual

Citation: ECOnGOOD Handbook for Organisations – Version 5.20, 2026, Matrix Development Team, International Federation for the Economy for the Common Good e.V

Licence: Workbook ECOnGOOD Balance Sheet 5.20 - Beta version © 2026 by International Federation for the Economy for the Common Good e.V. is licensed under Creative Commons Attribution-ShareAlike 4.0 International. To view a copy of this license, visit https://creativecommons.org/licenses/by-sa/4.0/

Licence: Workbook ECOnGOOD Balance Sheet 5.20 - Beta version © 2026 by International Federation for the Economy for the Common Good e.V. is licensed under Creative Commons Attribution-ShareAlike 4.0 International. To view a copy of this license, visit https://creativecommons.org/licenses/by-sa/4.0/

1.1 List of abbreviations and glossary

Welcome to the 5.2 version of the Common Good Balance Sheet Handbook. Before starting, please find below a list of abbreviations and a glossary.

In general, the glossary offered by EFRAG for the European Sustainability Reporting Standards (ESRS) is also used for this handbook. Some additional terms will be defined below, which are complementary to the ESRS one.

– Actions and measures – All initiatives and projects that an organisation carries out to ensure that it achieves its defined goals and targets. Actions and measures can already be fully implemented, initiated or planned.

– Active mobility – The collective term that encompasses all forms of transport that are based wholly or partly on muscle power; cycling and walking are the most prominent examples, but it also includes forms of mobility such as scootering and skateboarding, which may not immediately spring to mind.

- Balancer or balancing organisation - These terms are used to refer to the organisation using this handbook to write its Common Good Balance Sheet.

– Consensus – Approach to decision-making where everyone must agree to proceed. Any person can block a decision if they strongly disagree. The approach prioritises unanimity and collaborative agreement. Core question: “Do we all agree on this?”

– Consent – Approach to decision-making where a decision is accepted as “good enough for now, safe enough to try” even if not everyone fully agrees. Core question: “Is it safe to proceed? Do you object?”

– Fundamental human needs – According to economist and humanist Manfred Max-Neef, fundamental human needs are the finite, few, and universal requirements that all humans share — regardless of culture, era, or context. Unlike traditional models (like Maslow’s hierarchy), Max-Neef argued that needs are not hierarchical but interrelated and simultaneous. What differs across societies is not the needs themselves, but the ways (satisfiers) by which they are met.

– Goal – General, medium-long-term idea of the future or desired result that the organisation envisions, plans, and commits to achieve. A goal should not be confused with a target, an action, or a measure.

– Human development – Human development is about enabling people to live the lives they value by expanding their capabilities, ensuring equality, and promoting well-being and dignity for all. The concept was founded by economist Amartya Sen.

– Self-employed without personnel offering working time to the organisation – An individual who works under the direction of the organisation as a freelancer.

– Workforce – Includes both employees and self-employed without personnel offering working time to the organisation, independent of the type of contract.

– Systemic consensus – Approach to decision-making where, instead of voting for an option, participants indicate how much they resist or object to each option. The option with the least total resistance is chosen. The approach shifts the focus from agreement to minimising objection. Core question: “Which option causes the least resistance in the group?”

– Target – A precise, measurable outcome that an organisation aims to achieve within a certain timeframe as a milestone towards a broader and longer-term goal. A target should be drafted to be:

– Specific – (in what it desires to achieve),

– Measurable – (through KPI(s)),

– Achievable – (given resources, time, and skills),

– Relevant – (aligned with the overarching goal), and

– Time-bounded – (with a clear deadline or timeframe).

A target should not be confused with 'actions and measures'.

– Undertaking – Term used by the VSME standard for “organisation”. The term is only used in VSME datapoints.

# Glossary

- CGBS – Common Good Balance Sheet

- C.U. – Currency Unit

- FTE – Full Time Equivalent

- KPI – Key Performance Indicator

- T.T. – Temporal Trend

- PDCA – Plan Do Check Act

- VSME – Voluntary Sustainability Reporting Standard for Non-Listed Small and Medium Enterprises

# Abbreviations

1.2 Common Good Matrix and Common Good Balance Sheet

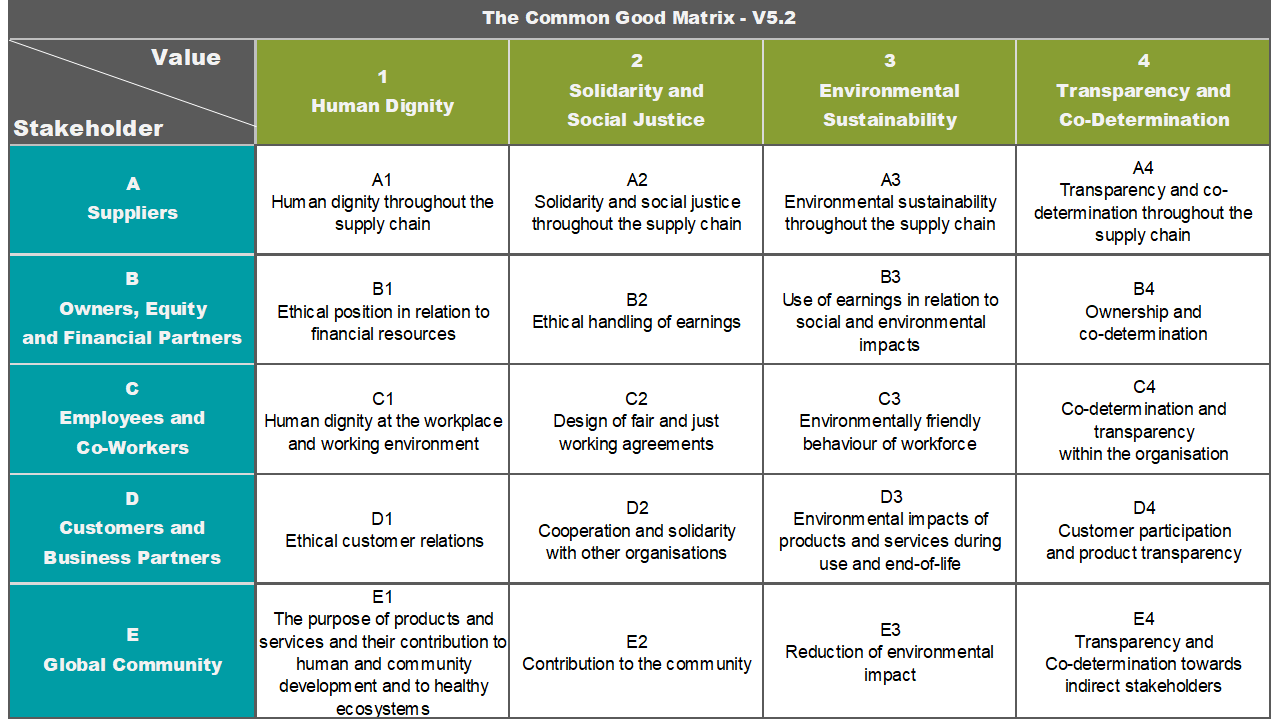

The Common Good Matrix is a 20 theme framework designed from the perspective of organisational processes for organisations willing to draft a Common Good Balance Sheet: an evaluation of business activities and a practical management-tool for organisational transformation towards the common good. The 20 themes, corresponding to the Matrix cells (e.g.: A1), are generated from the intersection between 4 value groups (columns) and 5 stakeholder groups (rows). Every theme is made of different sub-themes called aspects (e.g.: A1.1). Aspects can be positive, if they positively contribute to the Common Good, or negative, if they negatively contribute to the final Common Good assessment.

This handbook enables organisations to understand, evaluate, and prepare a Common Good Balance Sheet. It contains all you need to understand the themes and aspects of the Common Good Matrix. It is aimed for organisations, consultants, and auditors, but also for anyone interested to deppen the understanding of the Economy for the Common Good applied to organisations.

For each stakeholder group (row) the handbook offers a short introduction and some reporting questions and verification indicators useful for organisations to offer contextual and general information on each specific stakeholder group. The information gathered can be analysed under the lens of each value. This section helps to reduce repetition in the themes and aspects.

For each theme (cell) the handbook offers a short introduction, a list of behaviours typical of a common good oriented organisation for that theme (“An ECOnGOOD organisation…”), and some “Initial questions” thought to support internal reflection and discussion.

For each aspect (sub-theme), the handbook offers a short introduction, a list of reporting questions to guide the narrative reporting, a list of verification indicators to help the organisation identify the right level of evaluation and demonstrate that the right level/score is applied with evidence-based facts and figures, the levels of evaluation to guide the self-assessment and its external validation, and some “Guidance on indicators and evaluation” to support the assessment phase.

The main goal of a Common Good Balance Sheet is to evaluate an organisation's contribution to the common good by analysing its social and environmental impact and supporting the organisation to take actions within its field of influence, increasing the contribution to the common good but also improving its own resilience and strategy. This process encourages reflection on value-based business decisions and supports the organisation’s transformation journey through practical organisational development. The ultimate goal is to promote a common good orientation and to transform the economy.

For the ECOnGOOD movement, money and finance are just means. The goal is the common good. For this reason, the Common Good Matrix framework also invites some basic disclosure about the financial impact of an organisation’s social and environmental issues through some risk analysis questions and indicators.

A Common Good Balance Sheet is made of a Common Good Report and an Attestation.

The Common Good Report includes a narrative and data-based description of how the organisation’s activities relate to each of the 20 common good themes by answering the reporting questions and assessing the organisation according to the verification indicators laid out in this handbook. This will show how developed each value is within the organisation.

The ECOnGOOD Attestation documents the evaluation of each aspect, gives an overall score (Common Good Points), and presents results in the layout of the Matrix. A Common Good Attestation is awarded by a certified ECOnGOOD auditor.

Common Good Reports can be prepared by downloading the online version of this handbook in the reporting template version. Common Good Points can be calculated using the E-Calculator online at https://balance-sheet.econgood.org/.

1.3 Types of balance sheet

There are two types of Common Good Balance Sheet:

- CGBS only. This option is intended for organisations interested value-based reporting. It is a strategic and transformational tool that directs organisations towards the common good. This option does not cover the full VSME standard. It includes only those VSME indicators that support organisational transformation as mentioned above. Each aspect of the matrix shows the VSME indicators related to it. All indicators in the section: "VSME relevant indicators" shall be reported in order to complete the CGBS. When the "CGBS only" option is selected, these indicators will be displayed. In addition, users can select only mandatory datapoints - shall (CGBS and VSME are aligned in this categorisation).

- CGBS + VSME. This option is intended for organisations that wish to provide stakeholderswith sustainability information in line with the voluntary standard for small and medium-sized enterprises developed by EFRAG and endorsed by the European Commission (VSME), while strategically transforming itself towards the common good. Organisations choosing this option are expected to also disclose the "Extra VSME" datapoints, which are VSME datapoints not required under the "CGBS only" option. These are included in a dedicated section within each matrix aspect to ensure completeness of VSME reporting. Choosing this option means the display of ECOnGOOD’s original reporting questions and verification indicators plus “VSME relevant indicators” datapoints plus the “Extra VSME” datapoints. In addtional users can select basic or comprehensive module of VSME for display. This option enables full VSME coverage while using the value-based approach from the Common Good Framework as a strategic foundation for organisational transformation.

In case the “CGBS + VSME” option is chosen:

- All datapoints marked with “VSME” should be considered, though non-applicability and omission are always possible, if motivated.

- The user shall use the Euro as the currency for reporting.

- The organisation shall choose between Basic or Basic + Comprehensive Modules. The Basic Modules is the target approach for micro-undertakings (not exceeding two of the following thresholds: i. €450,000 in balance sheet total; ii. €900,000 in net turnover; iii. an average of 10 employees) and constitutes a minimum requirement and prerequisite for applying the Comprehensive Module.

By using the online ECOnGOOD html handbook it is possible to select which type of reporting to display for download.

All CGBSs completed with audit or peer validation are published in the ECOnGOOD database and are available to anyone. The balancer shall publish the CGBS on its website.

1.4 Preparing a report

In order to prepare the Common Good Report, the organisation should answer the reporting questions, verification indicators and VSME relevant datapoints provided in the handbook.

Reporting questions are thought to guide the narrative description of the context and the management approach through the disclosure of policies, measures, actions, and future goals and targets for each aspect.

Verification indicators are concrete facts and figures meant to demonstrate the effectiveness of common good-oriented transformation.

Policies might also be oral, especially in the case of micro-organisations whose culture is not often based on written documentation.

The handbook provides numerous reporting questions and verification indicators to encourage deep transformational reflection and evaluation in the greatest number of organisations, diverse in size, sector, and geography. This means that it is not expected that every organisation answers all datapoints. Datapoints are labelled with “shall”, “may”, or “if”.

“Shall” datapoints should always be answered. In case it is not possible, the “comply or explain” principle should be applied, using the “final datapoints sheet” provided.

“May” datapoints are optional. A selection based on relevance, depending on size, sector, geography, and, in general, risk assessment, is possible and encouraged. However, being completely optional, the “comply or explain” principle does not apply in this case.

“If” datapoints are mandatory only in specific cases, for instance, over a certain level of evaluation, or if applicable, or above a certain size threshold. If an “If” datapoint is applicable, the “comply or explain” principle should be applied, like in the case of “Shall” indicators. In all other cases, “If” datapoints correspond to “May” indicators.

Micro and small organisations often do not have extensive written policies or procedures, or do not conduct systematic, documented pilot tests or Plan-Do-Check-Act cycles. For these user typologies, it is sufficient to describe how the specific aspects are addressed. Also, these types of organisation might lack resources to commit to goals and targets for each ECOnGOOD matrix theme. The approach here is not to cover all themes with goals and targets but to start the transformative process, prioritising the most relevant ones. Lastly, they might choose to only focus on “Shall” and “If” questions.

In order to make the report lighter, it is not necessary to explain reasons for omission, non-applicability, or non-relevance in the narrative report. This means that it is enough to skip the question or indicator if the organisation does not want or need to answer it. A final “datapoints sheet” provided by ECOnGOOD here shall be used to note down reasons for omissions or any other notes. This sheet will be useful both internally as a final checklist, for ECOnGOOD auditors, and for users reporting under the CGBS + VSME option. In fact, the VSME standard explicitly requires organisations to state any omission of classified or sensitive information. If no data is available for verification indicators, other appropriate indicators can be used, and the reason why they were used should be explained.

In addition to the verification indicators, the organisation makes its own decision regarding what content to include and how detailed this should be. It should, however, be presented clearly and comprehensively using the SMART Principles (Specific, Measurable, Assignable, Realistic, and Time-bound) wherever possible to facilitate the subsequent audit of the report. In general, the organisation shall report information that is relevant, faithful, comparable, understandable, and verifiable. Every user is free to choose which currency to express financial figures in. However, since the E-Calculator weighting is based on some indicators expressed in euros, organisations reporting with other currencies should translate the relevant E-Calculator indicators into euros. This should be done using the average exchange rate over the reporting period.

Verification indicators might be asked in terms of trends. When this is the case, indicators are marked with the abbreviation “T.T.”, standing for “Temporal Trend). For all CGBSs after the first one, the trend over time is reported starting from the year when the datum is available (from the first year when a datum is available, even if this is before the first year of reporting). Trends shall be used for VSME indicators (in case of CGBS compliant with VSME reporting option), outcome/impact indicators (that is, indicators assessing effective transformation or positive change), and are recommended for any relevant indicator.

Auditors ensure that quality standards of reports are met and comparability is maintained. They can also request more detailed information.

The ECOnGOOD audit or peer assessment shall be repeated every two years. However, annual common good reporting is highly recommended to give a good pace to transformation and to align with normal business management timing. In case annual reporting is chosen, the ECOnGOOD audit can be repeated every two years, and the report for the non-audit year can also be published in the form of a delta report, only focusing on changes compared to the previous reporting period. For organisations who want to be compliant with VSME, it is sufficient to report on VSME indicators annually, though annual an Common Good Report is also recommended in this case.

Balancing organisations can also request a “Delta Audit”. In this case, the organisation is given the possibility to highlight changes in the current report compared to the previous one by marking them, thereby reducing the audit effort. However, a full report should still be published in the end.

Clearly, both a delta report and a delta audit are only possible within the same Matrix version.

The organisation should decide whether to report by calendar or financial year. Disclosed information should be consistent with the financial statement and prepared for easy cross-referencing.

The CGBS is generally prepared on an individual basis. However, a consolidated version can be considered if the reporting organisation has centralised processes for human resources management, purchasing, financial planning, and, in some cases, customer service. However, this must be considered on a case-by-case basis with the assigned ECOnGOOD auditor.

1.5 Evaluating the impact on the Common Good

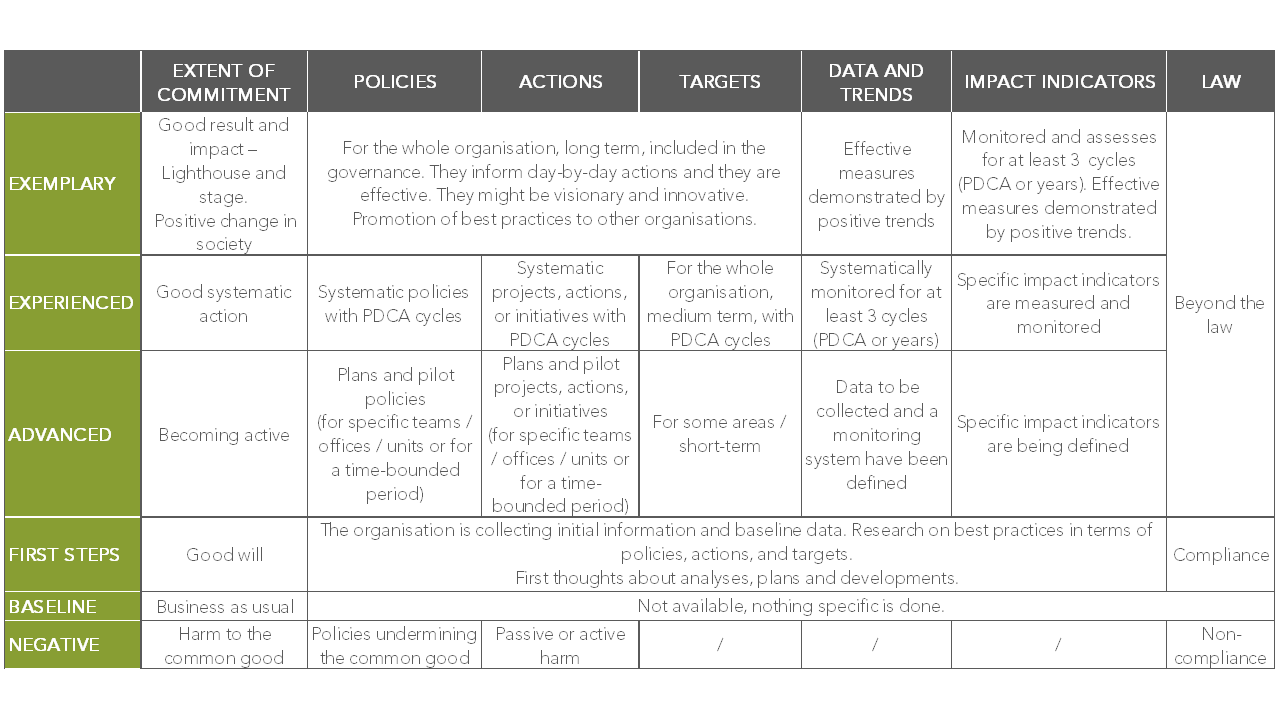

The purpose of the evaluation is to assess the impact of an organisation’s activities on the common good. As part of the process, the organisation places itself along a scale from baseline to exemplary. This is not, however, intended to be a measurement, but rather a means of using Common Good Values to assess an organisation’s activities and the impact they have on each of the stakeholder groups of the matrix.

The evaluation will be made for each aspect according to the “Levels of evaluation” section proposed in each aspect. The levels of evaluation include 5 levels of evaluation: Baseline, First Steps, Advanced, Experienced, and Exemplary. The criteria for each is described according to each aspect whilst being based on general levels of evaluation, as in the table below. In case of inconsistencies between aspect-specific levels of evaluation and the general ones, the latter prevails.

A baseline is given for all aspects, which describes business as usual when the topic is not reflected on. The evaluation process is informed by reporting questions and verification indicators. Moreover, the section “Guidelines for indicators and evaluation” within each aspect offers more information and interpretation guidelines to help with the evaluation process.

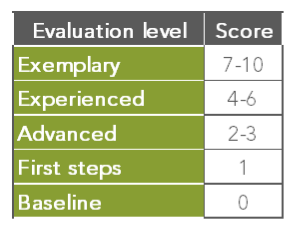

The association with a level of evaluation involves adhering to all relevant information and indicators and viewing them as a whole. Each level builds on the previous one, and achievement of the previous level is a prerequisite for a higher level. For example, to be awarded the level of experienced, all criteria under advanced must be met. This rule, however, is to be interpreted pragmatically. Minor discrepancies do not necessarily lead to a level downgrade. Each evaluation level is given a score depending on how common good driven the theme is within the organisation, and the extent to which the criteria for each level have been met.

Every aspect is rated on a scale from 0 to 10 and is weighted according to its relative importance within each theme (low/medium/high/very high).

Scores are recorded using the E-Calculator. This is a simple, automated aggregation of all the scores of each aspect according to their relative weighting. The more important an aspect is for the common good, the greater its overall value within the theme. The overall value of a positive aspect is rated on a scale from 0 to 10. The maximum value for a negative aspect is -200.

The final score is the weighted sum of each theme’s individual score.

The Common Good Matrix allows for a degree of flexibility, so that companies and organisations can make their own contribution to their ongoing development. You are encouraged to identify your own ways and means to implement Common Good Values. The Matrix provides specific guidance for all themes and aspects. This includes clear aims (e.g. ‘consensual decision-making within the organisation’) and offers examples of how to implement these (e.g. ‘systemic consensus’). It is possible, however, for organisations to develop their own comparable implementation steps. In this way, organisations are given room for creativity, and common good auditors are given leeway in the evaluation process.

1.6 Allocating Common Good Points

In addition to evaluating each theme, an overall evaluation is made by allocating Common Good Points. These Common Good Points may be important in the future concerning legal consequences and benefits arising from publishing an audited Common Good Balance Sheet. The maximum number of Common Good Points that can be scored is 1,000; the minimum is a negative score of -3,600. The Common Good Balance Sheet was developed for use by organisations in any sector, and of any size and legal structure - from non-profit organisations and small and medium-sized family businesses, right up to listed organisations and academic institutions. These organisations play very different roles within society, so the potential and effective impacts associated with their respective activities are also different. A variable weighting of themes reflects these differences in sector, scope, and scale of organisations.

As a starting point, each of the 20 themes is allocated an equal score of 50 points. To determine the overall score, the balance sheet calculator adjusts the weighting for each theme according to the following factors:

- The size of the organisation.

- Financial flows to and from suppliers, investors, and employees.

- The social impact of the raw materials in their country of origin.

- The sector and its associated environmental and social impact.

The total score that can be allocated remains the same, but the weighting of each theme is adjusted according to its relevance to the organisation. For detailed explanation about the functioning of the weghting system refer to this document.

1.7 New features of Matrix 5.2

Reports and evaluations prepared using version 4.1 or earlier versions of the Matrix are not directly comparable in terms of Common Good Score. The changes in Matrix Version 5.2 are designed to have little impact on the scoring in comparison with Matrix Versions 5.0 and 5.1. Some minor changes in the final scoring could still occur because questions and indicators are clearer, and, therefore, the evaluation could be affected as well.

Find below a list of major changes in Matrix 5.2:

- 2 types of reporting: “CGBS only” and “CGBS+VSME”.

- For standardisation purposes, this version of the matrix offers complete alignment with the VSME (For this reason, the word “undertaking” is used for VSME datapoints, while the handbook normally uses the word “organisation”). Therefore, all data points addressed by the VSME are presented as developed by EFRAG. Original datapoints from ECOnGOOD with similar content have been removed. Refer to the section on reporting options for more details.

- Old reporting template and E-Calculator datapoints are all integrated in the handbook to have everything in one place.

- Full/Compact versions are abandoned in favour of “Shall”/”May”/”If” tags applied both to reporting questions and verification indicators.

- The online digital handbook includes filters for: “CGBS only” or “CGBS+VSME" reporting options; VSME datapoints (Basic or Comprehensive); “Shall”/”May”/”If” datapoints.

- Levels of evaluation have been improved both by adding a general initial overview on the rationale behind them and working on aspect-specific ones. Specific adaptations have been completed to make the Baseline always applicable and to the Exemplary level.

- In order to reduce repetition, an intro has been added to each row with questions and indicators useful to provide a context to the whole row.

- A “Report introduction” section has been created to include general facts and figures, methodology, the Attestation, and a table with the prioritised goals and targets.

- VSME-inspired management approach questions have been consistently implemented in all aspects to report on policies, practices, measures taken, and future goals and targets.

- In order to make the CGBS more transformative, temporal trends have been introduced for some indicators and in the general levels of evaluation description for the highest levels, in addition to a table with prioritised goals and targets in the reporting introduction.

- It is now possible to report in any currency unit and is not obligatory in to report in euros.

- A final “datapoint xls sheet” (checklist) will make it fast and easy to monitor answered datapoints and to note down explanations for non-compliance with any datapoints.

1.8 ECOnGOOD Label

The ECOnGOOD Label is a comprehensive seal assessing the real impact of an organisation’s operations, management, and supply chains, providing a transparent evaluation based on the Common Good Matrix. It provides clear, evidence-based information, and offers real-time transparency through a QR code linked to the organisation’s Common Good Balance Sheet report and result.

There is strict criteria for eligibility:

- Payment of the association membership fees (or equivalent) in full to a national or regional ECOnGOOD Association.

- Possession of a valid Attestation (less than two years old).

- Completion of a Common Good Balance Sheet with an audited positive result.

- Registration in the ECOnGOOD audit database.

- Compliance with all publication requirements, included the publication of the Common Good Balance Sheet on the organisation's website.

- Validity of the contract between the organisation an the International Federation for the Economy for the Common Good e.V.

By meeting these requirements and displaying the ECOnGOOD Label, organisations demonstrate their commitment to sustainable and ethical practices, enabling consumers, investors, and policymakers to make informed decisions that support responsible business models.

2. Stakeholders

A. Suppliers

This group includes individuals, organisations, and companies supplying directly to the organisation, as well as indirect suppliers i.e. the entire supply chain. All products and services purchased from others are evaluated. Every organisation can take co-responsibility for its suppliers when making purchasing decisions, for example, by choice of suppliers, with contractual terms, and with some influence over its business partners.

How this shared responsibility is put into practice depends on the balance of power within the market and the distance between that link in the supply chain and an organisation. It is important to be especially alert to procurement procedures throughout the supply chain when buying products and services that have a significant commercial value for the organisation, are quantitatively important, or are high-risk components for an organisation’s products and/or services.

A list of the most important suppliers for an organisation and the products and services they provide can act as a guide for this. Important suppliers are those who deliver up to a total value of approx. 80% of the purchase volume, or 80% of purchase costs if volume is not available. Products and industries that carry a social or environmental impact (potential or effective) should be closely examined, even if the amount of purchase is small.

B. Owners and financial partners

Different types of organisations have legally different forms of ownership. Ownership of assets is associated with property rights and decision-making. These are protected and limited by constitutional, private, and public law. Forms of responsibility and liability are always associated with this. In the economy, private ownership by individuals commonly takes the form of sole ownership, as a personal partner, or as a shareholder in a corporation. Managing directors or the board of directors then assume ownership functions, accompanied by supervisory bodies. Similar forms are found in associations, self-governing bodies, co-operatives, steward-ownership, and companies owned by the workers. These representatives are obliged to act in the welfare of the organisations, taking into account the interests of the stakeholders, the restrictions imposed by the statutes or supervisory bodies, and the resolutions of general meetings. Under certain circumstances, personal liability may also arise.

We consider all financial market participants that provide financing and/or financial services to be financial partners, regardless of the type of products or services they offer. Here, the product type is deliberately not taken into account to avoid double-counting. In addition, most services are related to financing or the use of funds and are subject to the special conditions of the financial market.

C. Workforce

Stakeholder group C includes everyone who performs essential tasks for the organisation, is included in its regional, organisational, or social structures, and for whom at least one of the following criteria applies:

- People with whom the organisation has an employment relationship.

- People who have worked for the organisation for a period of at least six months.

- People who have worked for the organisation for at least four hours per week.

- People who are assigned tasks that are performed regularly and are recurrent (e.g. every summer).

Regarding external staff, it must be considered whether the organisation buys a service or buys working time. The former is stakeholder group A (suppliers), and the latter is stakeholder group C. Subcontractors who are deployed as personnel and work for and with the organisation and colleagues should be treated as internal staff when one of the mentioned criteria applies.

D. Customers and other organisations

Customers are the target group for a company or an organisation to buy or use their products and services. For example, customers of products and services, distributors, companies using the organisation’s product or service, contractors.

Other organisations (“competitors”) are organisations who may have the same (regional) target group and offer a comparable product or service. How an organisation behaves towards and interacts with others operating in similar markets is also taken into account.

E. Local and global community and ecosystems

Stakeholder Group E is defined more broadly than in the traditional business context. A common good approach recognises that everything in an ecosystem, economic system, or shared space in general, is interconnected, and that decisions and actions taken in one area can have far-reaching impacts on other areas.

Stakeholders in this sense are

- People: This is not about the people or groups directly affected (these are mentioned under stakeholder groups A to D), but about indirect dependents, future generations, and people in distant geographical areas, who may be indirectly and adversely affected by decisions.

- Local communities where the organisation operates.

- Animals: All animal species can be considered stakeholders if human activities affect their habitats or wellbeing.

- Plants and other life forms: Plants and microorganisms play a crucial role in many ecosystems and can be affected and threatened by human interventions.

- Ecosystems and natural habitats: Whole ecosystems, such as forests, oceans, rivers and deserts, can be considered stakeholders because they support the lives of numerous species and are central to ecological balance and the climate.

- Abstract or non-physical entities: Artefacts, cultural or spiritual values, traditions or concepts could also be considered stakeholders, especially if human activities affect these intangible aspects.

- The physical environment: Aspects such as air, water, and soil that may be altered or polluted by human activities.

In general, E row encompasses all those stakeholders that do not have a direct relationship with the organisation. This might also include employee families, for instance.

3. Values

The common good: A timeless value across borders

The common good is our founding value and principle. It is much older and broader than the relatively younger terms “sustainability” and “wellbeing”. It is deeply anchored in state theory and constitutional law due to its long historical backtrack. The philosopher Claus Dierksmeyer writes: “From Aristotle via Thomas Aquinas, up to and including Adam Smith, there was a consensus that both economic theory and practice needed to be legitimated as well as limited by a certain overarching goal (Greek: telos) such as the “common good”” (2016: 35). Timo Meynhard adds: “There is no culture that does not know the value of the common good” (2016: 174). According to Encyclopedia Britannica, the “common good” is “that which benefits society as a whole”. It is not the simple sum of individual goods but an ethical, relational, and inclusive goal, which requires mutual care, trust, and a perspective that leaves no one behind (Zamagni, Bruni, 2004). In the view of the Economy for the Common Good, it is a combination of relational values (respect, empathy, care, cooperation) and constitutional values (human dignity, solidarity, social justice, ecological sustainability, democracy).

There are two different philosophical approaches that define what the common good actually includes. The first one,"substantial definition", associates the decision to a metaphysical or autocratic instance. The second one, the one the ECOnGOOD movement adheres to, states that the concrete content of the common good can only be defined - or "composed" - by all members of a democratic community; accordingly, we call for the participatory development of Common Good Products as the successors of GDP from which an ethical compass for businesses can be later derived. For the time being, we work with the most frequent constitutional values mentioned above: human dignity, solidarity, social justice, ecological sustainability, and democracy, as they enjoy the highest possible legitimacy since they are enshrined in our constitutions.

3.1 Human dignity

For us, human dignity means that every human being is equally valuable, worthy of respect and protection, and unique, regardless of origin, age, gender, medical treatments, religion, or other characteristics. Human dignity is an inalienable right and denotes a moral entitlement that every human being has the right to expect simply by being alive. Human beings, and ultimately all living beings, have a right to exist and are deserving of appreciation, respect, and esteem. The human individual stands above every material thing. The human being as a person is the focus and must not be treated as a commodity, for example, a means of production as a unit of labour. Human dignity is independent of the usefulness of a human to provide labour and is inviolable and unassailable. Human dignity is a fundamental principle that promotes respect for, and protection of, the rights, health, and wellbeing of all people. Human dignity should act as a guiding principle for action, “Act that you use humanity, whether in your own person or in the person of any other, always at the same time as an end, never merely as a means,” according to Immanuel Kant, from the Metaphysics of Morals.

3.2 Solidarity and social justice

Solidarity and social justice are closely related values, both aim at strong social cohesion and a fair and just society; based on the equal opportunities and equal rights of all humans, as well as non-exclusion. While solidarity is based more on voluntary action and motivation, justice is more a legal pillar of the social contract. More concretely, solidarity is based on a feeling of togetherness, which, from the ECOnGOOD point of view, means an attachment to people as a whole, rather than to a defined group, which is how the term has been interpreted historically. The word stems from the Latin term “solidus” which means firm or to stand together and not allow to be divided. Solidarity aims to ensure that no one is left behind or excluded. Solidarity manifests itself as a mutual and unselfish willingness to help in times of need, to overcome difficult situations, and to voluntarily co-operate with one another. Solidarity may also entail specific community-based obligations and liabilities when the collective assumes responsibility for the weak. Social Justice provides equal opportunities and equal rights for all members of society. Social Justice aims to ensure that no one is disadvantaged or excluded. Social Justice aims to achieve a fair distribution of goods, resources, power, opportunities, and obligations. Social Justice is accomplished through social and legal mechanisms, such as a just organisation of the economy, the state, and the design of the democratic system, including strong individual and collective rights. As a general rule, these provisions should be brought under the control of law.

3.3 Environmental sustainability

This value is about meeting today’s needs without compromising the ability of future generations to meet their needs. It concerns the complex interactions between humans, other living beings, and the environment, which provides the basis for their existence and life. Human activity can pose a significant threat to the environment, thereby threatening all life forms that depend upon it for their existence. ECOnGOOD organisations are expected to have a net-positive impact concerning (“Do more good”) and not only a sustainability mindset (“Do less bad”). It is important to consider that actions taken are often associated with social change, which can be positive or negative. This aspect is very complex, and there is much literature about it. We cannot possibly cover everything, but we want to highlight a few key topics to inspire discussions.

- Life cycle perspective: For products, assess the impacts of design, raw materials, production, packaging, transport, use, and end-of-life. For services, assess the impacts of resources needed to provide them (e.g. servers, hardware, travel, energy, etc.) as well as the impacts of how clients use the service (e.g. enabling mining or shipping). Risk and impact assessments are recommended.

- Circularity: Shift from a linear journey from creation to waste towards closed material and energy loops.

- Eco-efficiency: Reduce resources and pollution per unit of output. Negative rebound effects should be monitored: efficiency gains lower costs and may lead to higher production and, thus, more impact.

- Eco-effectiveness: Go beyond eco-efficiency by achieving an absolute reduction of ecological footprint.

- Sufficiency: Reduce impacts to ensure all can live well within planetary boundaries.

- It is furthermore important not to fall into traps, like the carbon tunnel vision, which prioritise climate change mitigation at the expense of other important environmental impacts (such as biodiversity loss, water, etc.).

3.4 Transparency and co-determination

Transparency is a prerequisite for stakeholders to be able to participate in decision-making. Transparency means the disclosure of all information relevant to the common good, including critical data such as the minutes of executive committee meetings, salaries, internal cost accounting, and recruitment and dismissal procedures. Co-determination of stakeholder groups aims to ensure that all individuals directly or indirectly affected by actions (or inactions) are involved in decision-making processes. All individuals or groups who are affected by decisions and actions, or by the lack of decisions and actions, or have a legitimate interest in them, should be included. This expanded concept of participation aims to enhance the legitimacy and quality of decisions by ensuring that all those affected are heard. Stakeholders should be able to voice their concerns, provide information, and participate in decision-making processes. This contributes to greater transparency, accountability, and broader acceptance of decisions. Stakeholder co-determination also promotes the idea of social justice and inclusive organisational policymaking. It allows previously marginalised groups to raise their voices and participate in decision-making. By involving all those affected, the goal is to establish a balanced power relationship and ensure that the interests of those who usually have less influence are also taken into account. Co-determination involves the participation of each stakeholder in the decision-making process. There are different levels ranging from information provision, consultation, and participation, to collaborative decision-making.

4. Report introduction

Find below a list of general reporting questions and indicators meant to offer an overview of the reporting organisation with some facts and figures, reporting information and methodology, CGBS results and future goals, and targets. When reporting, you can delete all instructions and only keep the relevant information. It is also possible to draft a text including all the relevant answers.

4.1 General facts and figures

Reporting questions

- (shall) Name of the organisation.

- (shall) Logo.

- (shall) The date of the first operating year.

- (IfApplicable) List of relevant legal non-compliance, incident, and/or fine related to environmental, social, and governance issues in the reporting period.

- (shall) List of the organisation’s main risks.

Verification indicators

- (shall) Profit/loss at the end of the reporting period (in C.U.).

- (shall) The undertaking shall disclose the key elements of its business model and strategy, including: (d) if the strategy has key elements that relate to or affect sustainability issues, a brief description of those key elements. Example

address Item 1 Item 1 – address Item 2 Item 2 – address Item 3 Item 3 – address

ECOnGOOD Relevant VSME Indicators

- B1.24.e.i: (e) the following information:

i. the undertaking’s legal form; - B1.24.e.vi: vi. country of primary operations and location of significant asset(s); and

- B1.24.e.vii: vii. geolocation of sites owned, leased or managed.

- B1.24.e.ii: i.i. NACE sector classification code(s);

- B1.24.e.v: v. number of employees in headcount or full-time equivalents;

- B1.24.e.iv: iv. turnover (in Euro);

- B1.24.d: The undertaking shall disclose:

(d) in case of a consolidated sustainability report, the list of the subsidiaries, including their registered address4, covered in the report; and - C1.47.a: The undertaking shall disclose the key elements of its business model and strategy, including:

(a) a description of significant groups of products and/or services offered; Exampletitle description turnover Item 1 Item 1 – title Beschreibung zu Item 1 (Holzbau GmbH). Item 1 – turnover Item 2 Item 2 – title Beschreibung zu Item 2 (Holzbau GmbH). Item 2 – turnover Item 3 Item 3 – title Beschreibung zu Item 3 (Holzbau GmbH). Item 3 – turnover - C1.47.d: The undertaking shall disclose the key elements of its business model and strategy, including:

(d) if the strategy has key elements that relate to or affect sustainability issues, a brief description of those key elements. Exampledescription Item 1 Beschreibung zu Item 1 (Holzbau GmbH). Item 2 Beschreibung zu Item 2 (Holzbau GmbH). Item 3 Beschreibung zu Item 3 (Holzbau GmbH). - B1.24.e.iii: iii. size of the balance sheet (in Euro);

Guidelines for indicators and evaluation

For “CGBS only” users:

- In case that an ECOnGOOD relevant VSME datapoint is asked in Euros, any currency unit can be used instead.

- When reporting the NACE code, please, also explicitly state the sector.

- Both number of employees in headcount and in full-time equivalents should be reported for, though the VSME datapoint allows to choose only one of the two.

- The list of subsidiaries or legally connected organisations is also required for the individual reporting option.

- when disclosing ECOnGOOD relevant VSME datapoint on "key elements of its business model and strategy, including: (d) if the strategy has key elements that relate to or affect sustainability issues, a brief description of those key elements", please, briefly describe what links the organisation to the Common Good)

Nace code identification Users can identify their NACE code using this European Union page.

Additional activities to foster the common good – the organisation is asked to briefly describe any other activities pursued in the reporting period to foster the common good that are not explicitly addressed in the themes of the report.

Life cycle approach – the organisation is asked to describe the whole life cycle of the main product or service categories from cradle to grave/cradle to evaluate relevant ecological impacts. The life cycle includes the following stages: design (A3/D3/E3): 1) raw material acquisition, 2) purchasing and procurement (A3), 3) transportation, 4) production (E3), 5) use (D3), and 6) end-of-life (D3 and E3). The organisation has to consider and disclose the Life Cycle of its main products and services, deciding which environmental aspects are relevant by taking into account their ability to control and/or influence them. This does not require a detailed life cycle assessment. A thorough consideration of the life cycle stages that can be controlled and/or influenced (ISO 14001 / EMAS) is sufficient, or of those stages where the environmental impact is significant. If the life cycle is not sufficiently described, this leads to a devaluation by one evaluation point in the themes A3, D3, and E3. Sufficient means that accurate information is given on at least 5 of the 6 stages for products and services, focusing on resources needed to offer the service and environmental impact in the use phase. Accurate information means disclosure of the organisation’s ability to control and/or influence these stages and naming the possible measures.)

4.2 Methodology and reporting information

Reporting questions

- (shall) Reporting period. Example

start date end date Item 1 Item 1 – start date Item 1 – end date Item 2 Item 2 – start date Item 2 – end date - (shall) Matrix version

- (shall) Type of balance sheet (CGBS only/CGBS + VSME).

- (ECOnGOOD+VSME) The undertaking shall disclose which of the following options it has selected: (i.) OPTION A: Basic Module (only); or (ii.) OPTION B: Basic Module and Comprehensive Module.

- (shall) Currency unit used.

- (shall) Engagement process.

- (shall) Contact person for this report.

ECOnGOOD Relevant VSME Indicators

- B1.24.c: (c) whether the sustainability report has been prepared on an individual basis (i.e. the report is limited to the undertaking’s information only) or on a consolidated basis (i.e. the report includes information about the undertaking and its subsidiaries);

- B1.24.b: (b) if the undertaking has omitted a disclosure as it is deemed classified or sensitive information (see paragraph 19), the undertaking shall indicate the disclosure that has omitted.

Extra VSME Indicators

- B1.24.a: The undertaking shall disclose:

(a) which of the following options it has selected:

i. OPTION A: Basic Module (only); or

ii. OPTION B: Basic Module and Comprehensive Module;

Guidelines for indicators and evaluation

- Engagement process – the organisation is asked to briefly describe the engagement process for the preparation of the CGBS: who led the process (roles/organisational units/stakeholders), doing which activities, using what channels (workshops, surveys, etc.), and at which levels of engagement (information, consultation, partnership, co-determination, etc.).

- The ECONGOOD data-points xls sheet can be used to mark omitted disclosures.

4.3 Common Good Balance Sheet results and improvement plan for transitioning towards an Economy for the Common Good

Reporting questions

- (shall) Peer/audit certificate (when issued).

- (shall) Prioritised goals and targets.

ECOnGOOD Relevant VSME Indicators

- C2.48: If the undertaking has put in place specific practices, policies or future initiatives for transitioning towards a more sustainable economy, which it has already reported under disclosure B2 in the Basic Module, it shall briefly describe them. The undertaking may use the template found in paragraph 213 for this purpose.

- C2.49: The undertaking may indicate, if any, the most senior level of the undertaking accountable for implementing them.

Extra VSME Indicators

- B6.26: If the undertaking has put in place specific practices, policies or future initiatives for transitioning towards a more sustainable economy, it shall state so. The undertaking shall state whether it has:

(a) practices. Practices in this context may include, for instance, efforts to reduce the undertaking’s water and electricity consumption, to reduce GHG emissions or to prevent pollution, and initiatives to improve product safety as well as current initiatives to improve working conditions and equal treatment in the workplace, sustainability training for the undertaking’s workforce and partnerships related to sustainability projects;

(b) policies on sustainability issues, whether they are publicly available, and any separate environmental, social or governance policies for addressing sustainability issues;

(c) any future initiatives or forward-looking plans that are being implemented on sustainability issues; and

(d) targets to monitor the implementation of the policies and the progress achieved towards meeting such targets. Exampledescription practices Beschreibung zu practices (Holzbau GmbH). policies Beschreibung zu policies (Holzbau GmbH). any future initiatives Beschreibung zu any future initiatives (Holzbau GmbH). targets to monitor Beschreibung zu targets to monitor (Holzbau GmbH).

Guidelines for indicators and evaluation

The Common Good Balance Sheet can help organisations in evaluating their activities and in their transformation towards the common good. As a practical management tool, this section is forward-looking and is intended to help the user link the assessment phase with the definition of goals and targets for improvement and to operationalise goals and targets with proper resources (financial, human, etc.) and power.

In the VSME context, “practices” may include, for instance, efforts to reduce the undertaking’s water and electricity consumption, to reduce GHG emissions, or to prevent pollution, and initiatives to improve product safety, as well as current initiatives to improve working conditions and equal treatment in the workplace, sustainability training for the undertaking’s workforce, and partnerships related to sustainability projects.

While specific policies, practices, strategies, measures, and future goals, targets, and actions have been described for each Matrix aspect, the recommendation here is to only focus on the main ones, as well as on prioritised goals and targets.

Prioritised goals and targets can be disclosed in tabular form. The following columns are suggested: Aspect/theme; long-term goal, related target(s) specific to the goal; identified KPI to measure that the target has been successfully achieved; year when the target will be met; ownership, and concrete finance and/or investment needed to achieve it might also be added. It is recommended to draft the prioritisation based on identified main risks – see 4.1 section indicator – and impacts.

5. Let’s start with organisational purpose

Organisations offer their employees a workplace, pay them fairly, and, thus, enable them and their families to earn a living. Organisations are part of society, and they can serve and advance society by fulfilling human needs or broader societal needs to foster well-being. Organisational purpose clarifies the reason why an organisation exists and does business, and the deep meaning that it has for the world. The organisational purpose clarifies what life improvements for all stakeholders (particularly society, the environment, and clients), now and in the future, an organisation is committed to. Defining the organisational purpose means being aware of one’s impact and managing it in the most positive way. An organisational purpose is the organisation’s overarching reason for existing.

A Purpose Statement is a tool to communicate and articulate purpose in a concise and inspirational way. It consists typically of one or two sentences that convey how the organisation fulfils human needs or solves human problems. A purpose statement can also present a risk if it is not actually lived as the core of the business strategy. For this reason, in the introduction section of each matrix row, the handbook offers some questions which can help organisations to reflect and describe how organisational purpose is actually lived in the organisation and in the relationships with all stakeholders. The following questions may seem more suitable for organisations with substantial impacts on society, but even for small organisations, they can help to have a clearer view. The questions help clarify how an organisation is embedded in its social, economic, and geographic environment, its sphere of influence, and what its responsibilities are.

How to report on Purpose

The questions and indicators considered relevant below can be answered in the introductory section of the report. The section should give a complete view of the reasons and motivations for why an organisation exists and how these influence strategies, actions, and results across the matrix themes. However, some answers are also recalled in other sections of the report, where it makes sense, and where it is helpful for the evaluation of the theme. It can be helpful for organisations to see the connection to the themes and how organisational purpose is put to action. Another useful tool for organisations at the beginning of their common good journey is the ECOnGOOD Business Canvas. It includes purpose and links to each row and can help initial reflections on purpose in connection with all ECOnGOOD values and stakeholders.

5.1 Organisational purpose

Reporting questions

- (shall) To which local, regional, or global challenge does the organisation offer a solution or a contribution towards a solution? Is this contribution part of the core business strategy or voluntary actions?

- (If_fromFirstSteps) Has the organisation ever thought of giving a broader sense to business itself by connecting its business to local, regional, or global challenges to contribute to an answer?

- (shall) What is the social, environmental, and economic role of the organisation through its business?

- (shall) How does the organisation’s business contribute to the needs of customers and stakeholders?

- (If_PurposeStatementExists) Does the purpose statement of the organisation explicitly set out the positive impact it has on stakeholder needs and aspires to have on future stakeholders?

- (If_OrgWithPurpose) Is the organisation’s business strategy developed and adapted based on the organisation’s purpose?

- (If_OrgWithPurpose) How does the organisation ensure that its purpose can be fulfilled during times of socio-economic stress?

- (If_PurposeStatementExists) When, and by whom in the organisation, was the organisational purpose developed, and when was it last amended? (Please report literally.)

Verification indicators

- (may) Purpose Indicator 1 in the reporting period (T.T.). Example

2025 2024 2023 Beispielwert Beispielwert Beispielwert - (may) Purpose Indicator 2 in the reporting period (T.T.). Example

2025 2024 2023 Beispielwert Beispielwert Beispielwert

Guidelines for indicators and evaluation

Indicators should be self-defined by the organisation. They should measure how the organisation’s behaviour in economic, social, and environmental contexts meets the purpose of the organisation over time. They should be understandable, measurable over time, and clearly related to your contribution. The indicators should relate to the output of your organisation (your service or product, and your internal organisational management) or to the outcome for society you aspire to. Note: An organisation chooses its purpose-indicators for their first ECOnGOOD balance sheet and in the next balancing periods the same indicators are used to monitor changes and improvements.

A. Suppliers

Suppliers are key stakeholders, enabling organisations that offer their products and services. Cooperation on different levels will be analysed in the A-Row, from positive aspects like transparency, cooperation, and joint development to negative aspects like hidden human rights infringements, externalised costs, and pollution. Each organisation’s sphere of influence and its scope vary depending on its size and other factors. With greater power comes a greater responsibility!

Find below a list of general reporting questions and indicators meant to offer an overview of the reporting organisation, with facts, figures, and methodology. If there is repetition of questions, choose the most appropriate place to report. Whenever possible, give practical examples/situations showing how values are lived in practice.

In the first analysis, please consider your most important direct suppliers, and in the second analysis, dive deeper into the supply chain, especially for items of high value, of critical environmental or social impact, or critical to offering your products/services. Please choose the most adequate reporting method, like directly from your organisation’s management tool (if available), and use tables, graphs, trends, and/or free text.

Reporting questions

- (shall) Which raw materials are used in the production process and in what quantity?

- (shall) Has the organisation performed an impact analysis of its supply chain? Please describe.

- (may) How are the organisation’s suppliers involved in product design?

- (may) How have the organisation’s suppliers changed local conditions, impacted the local community, and the environment?

- (shall) How much value is added by a specific supplier vs. what is the impact of their product/service (on environment, social, externalised, etc)

- (may) Is the purpose statement of the organisation communicated to suppliers?

- (may) Do the organisation’s suppliers share the same purpose?

- (may) Are there any action programmes to share and implement the organisational purpose with suppliers and/or the organisation’s supply chain, e.g. shared policies, code of conduct/ethics, agreements, etc.?

- (may) Does the purpose of the organisation entail global challenges related to supply chains, and does the organisation address these challenges in its supply chain policies?

- (may) Can the organisational purpose help to increase cohesiveness among partners in the supply chain, while respecting the peculiarities of organisations?

- (IfApplicable) Which certifications are available in the organisation’s supply chain?

- (shall) What policies and practices exist in the organisation regarding supplier selection and supply chain assessment?

- (shall) What strategies and measures have been put in place before (short-list) and during the reporting period, for direct suppliers and the whole supply chain?

- (shall) What results have been reached so far concerning suppliers and the supply chain? (If possible, evaluate the effectiveness of the actions taken.)

- (shall) What future goals, targets, and actions have been planned concerning suppliers and the supply chain? What are the main actions to achieve these targets?

Verification indicators

- (shall) Main geographic location of direct suppliers, expressed as a percentage of the purchase volume (T.T.). Example

2025 2024 2023 DE – Teil 1 10.6 72.4 32.9 DE – Teil 2 60.5 4.1 58.5 TOTAL 71.1 76.5 91.4 AT – Teil 1 45.9 63.1 86 AT – Teil 2 89.7 46.6 31.8 TOTAL 135.6 109.7 117.8 CH – Teil 1 28.7 43.9 73.1 CH – Teil 2 33.7 70.4 71.9 TOTAL 62.4 114.3 145 UK – Teil 1 39 40.7 69.6 UK – Teil 2 70 24.2 41.5 TOTAL 109 64.9 111.1 US – Teil 1 86.6 62.4 19.4 US – Teil 2 14.2 84.7 64.5 TOTAL 100.8 147.1 83.9 - (shall) Country of origin of goods/services/raw materials, expressed as a percentage of the purchase volume. Please go as far back in the supply chain as feasible (T.T.). Example

2025 2024 2023 DE 70.4 7.1 34.4 AT 13.6 86.6 78.4 CH 68.2 32.2 12.8 UK 6.2 13 65.7 US 72.4 36.7 61.6 - (may) Percentage of purchased products, services, and raw materials for which the supply chain can be traced back to the origin, out of the total procurement volume.

- (shall) Total purchases from suppliers.

- (shall) Enter the 5 most important industry sectors whose products or services you use. Example

countryCode industryCode costs Item 1 Item 1 – countryCode Item 1 – industryCode Item 1 – costs Item 2 Item 2 – countryCode Item 2 – industryCode Item 2 – costs Item 3 Item 3 – countryCode Item 3 – industryCode Item 3 – costs

ECOnGOOD Relevant VSME Indicators

- C1.47.c: The undertaking shall disclose the key elements of its business model and strategy, including:

(c) a description of main business relationships (such as key suppliers, customers distribution channels and consumers);

Guidelines for indicators and evaluation

- Suppliers considered in A-Row can be suppliers of material and services. Suppliers related to finance/ money and insurance will be considered under the B-Row

- If helpful suppliers can be clustered into a) infrastructure, b) core-processes, c) support-processes, d) administration in order to allow focus on: greatest leverage, possibility of action and change

- Please consider the main suppliers, which could e.g. be the ones providing 80% of the purchase volume or expenses. Alternatively focus could be on the top 10 suppliers and consider how much purchasing volume/expenses these cover.

- Products and industries that carry a high social or environmental risk should be closely examined, even if the amount of purchase is small.

- As mentioned in the general intro, whenever possible, please note down potential actions and targets in the SMART format and then prioritise them.

- Specifically for the supply chain, it may be important to distinguish between items hard to change (like infrastructure) and where change is possible through conscious purchasing, supported by criteria and a strategy.

- Do the policies, practices, and future initiatives aim to reduce negative and enhance positive social and environmental impacts? e.g.: human rights, climate change, pollution, water and energy resources, biodiversity, and the circular economy (VSME - principles of preparation).

- An impact analysis could consider accidents, likelihood of disruption, availability of alternative suppliers, transition events like climate change, stakeholder perceptions, pricing, etc.

- Purchasing criteria: e.g. standards, certificates, surveys, visits, audits, etc. It may be important to make a two-way assessment and look at supplier satisfaction with your organisation’s practices, conditions, etc., as well as compliance with their own promises.

- Product design could cover areas like continuous improvement, cradle-to-cradle, circular economy, etc.

- Please answer the above questions for your direct suppliers and then your indirect suppliers. In A2 and A4, there is a specific aspect for this; in A1 and A3, there is not, since, unfortunately, that couldn’t be standardised for this workbook.

- Some indicators may be hard to accurately measure (and express as percentage for example), in this case please make an estimation and be clear about the underlying premisses.

A1 Human dignity throughout the supply chain

All goods and services purchased by an organisation have an associated impact on society, which can be either positive or negative. One of the most important aspects is the working conditions along the entire supply chain and the impact on local communities. An organisation is co-responsible for the well-being of their direct and indirect suppliers, their workers, and communities.

An ECOnGOOD organisation...

- purchases goods and services that are provided under ethical and fair conditions.

- is alert to impacts throughout the supply chain, where the violation of human dignity is a common occurrence.

- actively promotes behaviour that improves human dignity throughout the supply chain.

Initial questions

- What do we know about our suppliers‘ commitment to respecting human dignity, especially that of our key suppliers?

- What potential negative impacts exist throughout the supply chain concerning the violation of human rights that relate to our business activities?

- How does our organisation contribute to the implementation of ethical and fair working practices, and how do we help to solve problems and meet challenges throughout the supply chain?

A1.1 Ethical working conditions in the supply chain

Organisations should be actively involved in how the goods and services they purchase are created and provided. In the first analysis, please focus on your direct suppliers and in the second step focus on the entire supply chain.

Reporting questions

- (shall) What are the criteria related to ethical working conditions for selecting suppliers?

- (shall) How are impacts related to ethical working conditions in the supply chain assessed?

- (IfApplicable) What influence is exerted on suppliers to ensure they respect the human dignity of all their stakeholders?

- (IfApplicable) Please detail your analysis regarding the management questions from the intro about existing policies and practices, as well as strategies and measures, results reached, and future goals, targets, and actions for this aspect of ethical working conditions.

- (may) How does your organisation evaluate the integration of key suppliers into their local communities?

Verification indicators

- (shall) Percentage of purchased goods and services produced under fair and ethical working conditions out of total purchased goods/services in the reporting period (T.T.). Example

2025 2024 2023 54.94 32.64 58.95

Levels of evaluation

Exemplary: Ethical supply management is part of the organisation’s corporate identity and positioning. Effective (and possibly innovative and/or visionary) procedures for ethical sourcing have been considered in all areas of business.

Experienced: Comprehensive purchasing guidelines have been established, outlining how suppliers are assessed, selected, and supported in implementing required fair and ethical conditions. Almost all key suppliers have above-average working conditions.

Advanced: Initial measures to ensure the fair and ethical working conditions of direct suppliers have been established. The supply chain is evaluated in the most critical parts and/or for the main indirect suppliers with regard to fair and ethical working conditions. Initial exclusion criteria are met when making purchases.

First Steps: Information is being gathered about how to assess direct suppliers according to their working conditions. Criteria and strategies for improvement are being discussed.

Baseline: Business as usual, no specific impact assessment/analysis for this aspect.

Guidelines for indicators and evaluation

A1 and A3 do not have a separate aspect considering the whole supply chain, as have A2 and A4. Therefore, please still perform this analysis, but within the existing aspect.

Purchasing behaviour should be evaluated according to exclusion criteria, positive criteria and/or processes. The following criteria will be evaluated in different aspects:

- The extent to which direct suppliers have implemented working practices that promote human dignity (C1).

- The extent to which suppliers purchase from sources that respect human dignity (A1).

- How ethical suppliers’ approaches are when handling funds and interacting with clients (B1 and D1), and whether the social impact of their goods and services contributes to the common good (E1).

The following aspects may help when preparing a self-evaluation:

- Great importance should be attached to any process in the supply chain that is associated with a high social impact. If organisations in critical supply chains operate significantly above current standards, this scores positively when determining the level of evaluation.

- Any significant impact on society may not lie directly with the supplier, but much earlier in the supply chain. Attention should be focused on where the impact is greatest.

- As an organisation grows, its procurement management policies become increasingly important. The longer the supply chain, and the greater the impacts associated with it, the higher the standards must be.

- Strong integration of suppliers in local communities can help to improve working conditions and generate lasting local positive impact.

- Smaller organisations are not expected to have individual impact assessment investigations for the supply chain, but should systematically assess publicly available information to identify violations to human dignity in the supply chain.

A1.2 Negative aspect: Violation of human dignity in the supply chain

Significant problems related to working conditions can be associated with the production of many goods that are used on a daily basis. If one takes into consideration global, complex production processes, it is almost impossible for organisations and individuals to completely exclude all violations of human dignity.

Reporting questions

- (shall) Which steps in the supply chain pose a particular threat to human dignity?

- (may) How are violations of human dignity in the supply chain identified?

- (shall) What measures are being taken to reduce these impacts?

- (shall) What measures are being taken to prevent these impacts?

- (IfApplicable) If the organisation has been convicted or fined, what measures have been taken to avoid new convictions and fines in the future? How is the effectiveness of these measures assessed?

- (IfApplicable) Has the organisation conducted due diligence to ensure it complies with all relevant laws?

Verification indicators

- (shall) Percentage of purchased goods and services that present risks related to human dignity (out of the total volume of purchased goods/services).

- (IfApplicable) Number of convictions and fines on specific law non-compliance on this aspect in the reporting period.

ECOnGOOD Relevant VSME Indicators

- C7.62.c: Severe negative human rights incidents

(c) Is the undertaking aware of any confirmed incidents involving workers in the value chain, affected communities, consumers and end-users? If yes, specify.

Levels of evaluation

- Baseline: The organisation has low impacts in its supply chain and/or reduces any potential negative social impact to a minimum.

- 20 negative points: The organisation obtains goods and services from questionable/untransparent sources. The measures taken so far are not sufficient to adequately mitigate the negative social impacts.

- 50 negative points: The organisation has been convicted or fined for specific law non-compliance on this aspect in the reporting period.

- 100 negative points: The organisation obtains essential goods and services from questionable/untransparent sources, and has made little effort to introduce measures to improve this.

- 200 negative points: The organisation’s business practices contribute significantly to negative impacts on ethical working conditions in the supply chain.

Guidelines for indicators and evaluation

Attention should be focused on those goods and services that significantly risk violating human dignity. Impacts can stem from their point of origin (e.g. they are sourced from countries with low standards) or from the industry sector itself. Most individuals and organisations purchasing electronic goods and batteries probably have an (involuntary) negative impact, also caused by a lack of transparency in a highly complex supply chain. Please distinguish between items hard to change (like infrastructure), and assign fewer negative points, and where change is possible through conscious purchasing supported by criteria and a strategy, and apply negative points more strictly.

A2 Solidarity and social justice throughout the supply chain

Today‘s economic activity is frequently characterised by predatory pricing, selfish efforts to maximise market power, and, in global supply chains, by exploitative business and working practices. Organisations are responsible for fair and just interactions when dealing with their direct suppliers and, within their scope to exert influence, throughout their entire supply chain.

An ECOnGOOD organisation...

- ensures that business relations with their direct suppliers are fair and just.

- recognises its co-responsibility for solidarity and social justice throughout the supply chain, and develops its business practices accordingly.

Initial questions

- In which areas do direct and indirect suppliers expect fairness and solidarity from us?

- To what extent do our direct and indirect suppliers behave with fairness and show solidarity towards their stakeholders?

- What is our level of influence along the supply chain, and what can we do to create a positive impact?

A2.1 Fair and just business practices towards direct suppliers

It is essential that the organisation commits to a fair distribution of added value along the supply chain, ensuring economic security for all involved. Fair and equitable business practices around pricing, payment terms, delivery conditions, payment period, payment behaviour, delivery reliability and timeliness, behaviour in the event of faults, liability conditions, guarantee and warranty conditions are practical examples.

Reporting questions

- (shall) How does the organisation define fair and equitable business relationships and practices with its key direct suppliers?

- (may) What measures or sanctions are in place in case of violations?

- (IfApplicable) How satisfied are the organisation’s suppliers with regard to pricing and terms of payment and delivery, as well as with their share of added value? How is this evaluated?

- (may) Assessment of the organisation’s market power. Market power can be used for positive or negative influence. Please analyse the real or potential positive impacts.

- (IfApplicable) Please explain the analysis conducted in detail regarding the management questions from the intro about existing policies and practices, as well as strategies and measures, results reached, and future goals, targets, and actions for this aspect of fair and just business practices towards direct suppliers.

Verification indicators

- (shall) Average duration of the business relationship with direct suppliers out of the number of active years of the organisation (T.T.). Example

2025 2024 2023 Beispielwert Beispielwert Beispielwert - (shall) Percentage of relevant direct suppliers who are satisfied with the business relationship and perceive it to be fair in the reporting year (T.T.). Example

2025 2024 2023 18.47 75.25 71.99 - (shall) Percentage of all goods and services purchased from suppliers/producers locally and regionally (T.T.). Example

2025 2024 2023 locally – Teil 1 24.5 48.4 53 locally – Teil 2 63 49.8 46.5 TOTAL 87.5 98.2 99.5 regonally – Teil 1 11.6 44.3 12.1 regonally – Teil 2 14.2 21.5 61.7 TOTAL 25.8 65.8 73.8 country – Teil 1 59.4 69.2 12.2 country – Teil 2 0.3 37.2 70.8 TOTAL 59.7 106.4 83

Levels of evaluation

Exemplary: Fair business relationships, based on strict ethical principles, have been established with all direct suppliers. The average duration of the relationship with direct suppliers is at least ten years (or 80% of the organisation’s existence time for start-ups), and/or all key direct suppliers are very satisfied with pricing and terms of payment and delivery, as well as with the distribution of the added value through the supply chain.